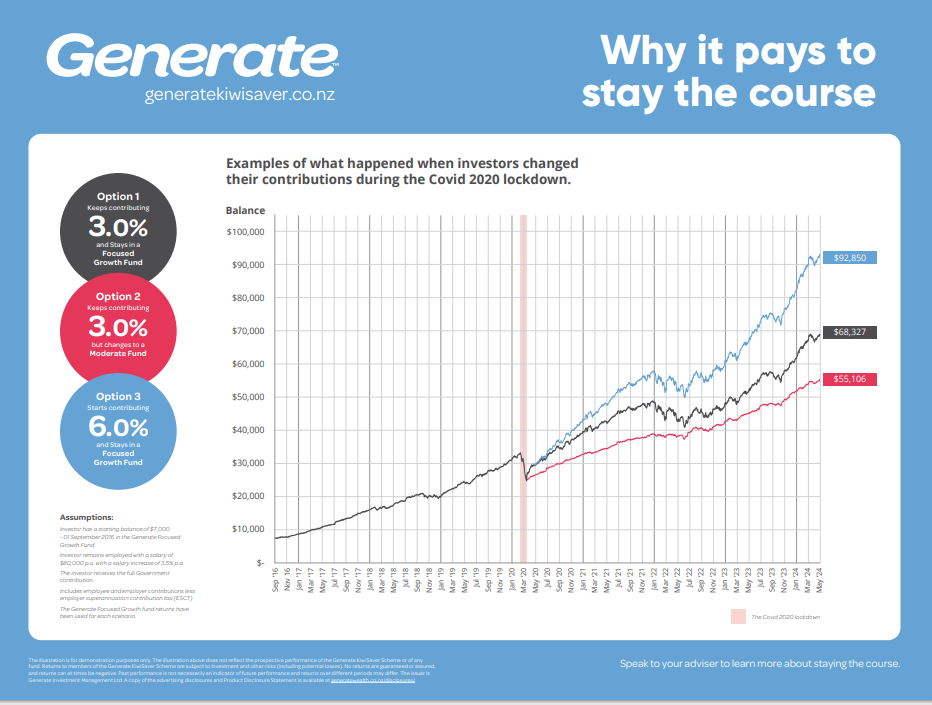

KiwiSaver and Risk: Why Higher-Risk Funds Can Pay Off in the Long Run

When it comes to KiwiSaver, one of the most important choices you can make is deciding what type of fund to invest in. Should you go with a conservative, balanced, or growth fund? The answer depends on your goals and how far away you are from needing the money. For most people in the early stages of their savings journey a higher-risk fund can deliver better returns over time.

Here’s why higher-risk KiwiSaver funds can benefit your long-term savings, and when it might make sense to temporarily switch to a lower-risk option.

Understanding KiwiSaver Fund Types

KiwiSaver providers offer different types of funds with varying levels of risk:

Conservative funds invest mainly in cash and bonds. They’re low risk, with small returns and less chance of sudden drops in value.

Balanced funds mix shares, bonds, and other investments. They have moderate risk and moderate returns.

Growth and aggressive funds invest more heavily in shares. These have higher risks and greater potential for higher long-term returns.

In general, the more risk a fund takes the more it can grow over time (but the more it can also fluctuate!).

Why Higher-Risk Funds Can Be a Smart Long-Term Strategy

If you’re in your 20s, 30s or even 40s, and not planning to withdraw your KiwiSaver for decades, a higher-risk fund can help your savings grow faster. Over long periods growth funds typically outperform conservative ones because they take advantage of the share market’s long-term upward trend.

Yes, you might see your balance drop during times of market volatility but, if you’re not withdrawing your money anytime soon, there’s time to recover and gain more in the long run.

Even small differences in returns can add up to thousands of dollars by the time you reach retirement. That’s why staying in a higher-risk fund for most of your working life often makes sense.

When to Dial Back the Risk

There are times when switching to a lower-risk fund is a smart move even if you’re usually invested in growth:

If you’re about to use your KiwiSaver to buy a first home: it’s wise to move to a conservative fund 6–12 months before settlement. This protects your balance from sudden market dips that could reduce your deposit right when you need it.

As you approach retirement: it's common to gradually reduce the risk in your fund. This helps protect your savings from large market drops just before you plan to use them.

Think of it like this: early in life your KiwiSaver is all about growth. But as you get closer to using the money — whether for a home or retirement — your focus shifts to stability.

After Buying a Home: Consider Moving Back to Growth

Once you’ve used your KiwiSaver to buy your first home, and the immediate risk of needing the money has passed, it often makes sense to move your funds back into a higher-risk portfolio. The goal is to take advantage of the long runway until retirement and let your savings grow again.

You’ll still want to review your fund every few years, especially if your circumstances change. For most people higher risk in the early and middle stages of KiwiSaver pays off.

Long-Term Gains Come from Long-Term Thinking

KiwiSaver isn’t just a savings account — it’s an investment plan that works best when you take the long view. Staying in a higher-risk fund for most of your working life can give your money more time and potential to grow.

Yes, there will be bumps along the way. Markets go up and down. But history shows that, over time, the trend is upward. Your KiwiSaver balance is likely to benefit if you stick with a growth-focused approach until it's time to reduce risk closer to retirement.

A little risk now could mean a much more comfortable retirement later.