Featured

Health insurance helps cover medical costs like doctor visits, hospital stays, and prescriptions, making healthcare more affordable. By choosing the right policy and understanding how it works, you can ensure quicker access to treatment and greater peace of mind for you and your family.

Buying your first home can feel overwhelming, especially when it comes to understanding mortgages. By learning the basics—like the types of mortgages, interest rates, and borrowing limits—you can confidently make informed decisions on your journey to homeownership.

Budgeting doesn't need to be complicated—even if numbers aren't your thing. Using simple strategies like the 50/30/20 rule, automating savings, and allowing yourself a guilt-free spending allowance can make managing money stress-free and achievable.

Budgeting doesn't need to be complicated—even if numbers aren't your thing. Using simple strategies like the 50/30/20 rule, automating savings, and allowing yourself a guilt-free spending allowance can make managing money stress-free and achievable.

Buying your first home can feel overwhelming, especially when it comes to understanding mortgages. By learning the basics—like the types of mortgages, interest rates, and borrowing limits—you can confidently make informed decisions on your journey to homeownership.

Managing debt doesn’t have to feel overwhelming. By understanding what you owe, creating a structured repayment plan, and making mindful financial choices, you can take control of your finances and work towards a debt-free future with confidence.

Buying your first home is exciting, but common mistakes like not setting a budget, skipping inspections, or rushing the process can lead to costly regrets. With careful planning and the right advice, you can avoid these pitfalls and make confident, informed decisions on your home-buying journey.

Investing in property can be a powerful way to build wealth, generate passive income, and secure your financial future. By understanding key factors like location, rental yield, and financing options, first-time investors can make informed decisions and avoid common pitfalls.

Making a medical insurance claim doesn’t have to be stressful. By understanding your policy, gathering the right documents, and following the correct process, you can ensure a smooth and successful claim while avoiding common mistakes.

Saving for a house deposit can feel overwhelming, but with smart budgeting, KiwiSaver benefits, and disciplined saving habits, you can reach your goal faster. By cutting unnecessary expenses, automating savings, and exploring government assistance, homeownership may be closer than you think.

Teaching kids about money from a young age helps build confidence and lifelong financial skills. With simple tools like pocket money, real-life conversations, and goal setting, parents can prepare their children to make smart financial choices as they grow.

If you’re in KiwiSaver, the government may be offering you up to $521.43 each year—no strings attached. The Member Tax Credit is one of the easiest ways to grow your savings, but you need to contribute the right amount to get the full benefit.

If you're buying your first home, your KiwiSaver could be the key to getting on the property ladder. Withdrawing your savings for a deposit is possible after just three years of contributions—making that big step a little more achievable.

From 1 April 2025, PIR tax bands are changing—and getting your rate right could save you money. This guide explains what PIR is, how to calculate it, and why it matters for your KiwiSaver earnings.

If you're planning to use your KiwiSaver for a house deposit, now's the time to think about stability. Switching to a conservative fund can help protect your balance from market dips and give you peace of mind when it matters most.

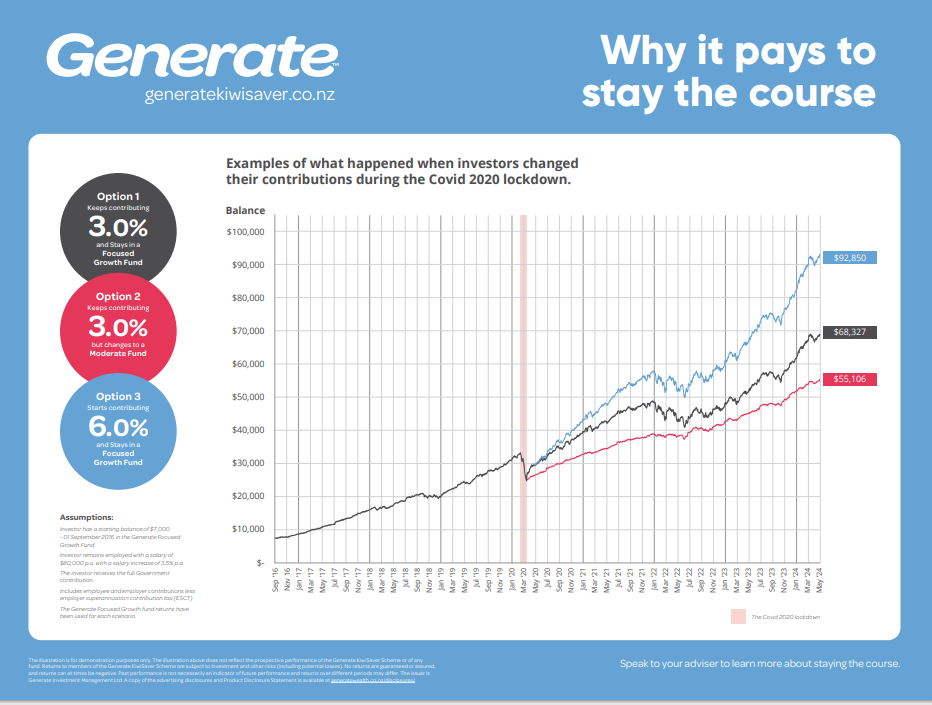

If you’re not planning to use your KiwiSaver for a while, staying in a higher-risk fund could help grow your savings faster. With more time to ride out market ups and downs, the long-term rewards often outweigh the short-term risks.

Split banking means spreading your lending across more than one bank to improve control, protect your savings, and reduce risk. It’s a simple strategy that can offer big benefits—especially if you value financial flexibility.

Helping your child buy their first home can be incredibly rewarding—but it’s not without risks. From gifting money to acting as a guarantor, this guide covers the common pitfalls and smarter ways to offer support while protecting everyone involved.

KiwiSaver isn’t just for adults—setting one up for your child can give them a powerful head start on their financial future. With time on their side, even small contributions can grow into something significant thanks to the power of long-term investing.

When you’re taking out insurance, choosing the right excess can make a big difference to your premiums. A higher excess usually means lower monthly costs—but it’s important to understand how this works and when it might be the right choice for you.

Your insurance needs change as your life changes—and without regular reviews, you might end up paying too much or not having enough cover when you really need it. Taking time to review your insurance helps you stay protected and can even save you money.

Before you start house hunting, it’s important to know exactly how much you can afford to borrow. A home loan pre-approval doesn’t just give you a number—it gives you confidence, focus, and a realistic understanding of your buying power.

If you're young and in good health, life insurance might not seem like a priority—but that's exactly when it can be most affordable and easiest to get. Starting early can give you peace of mind, financial security, and protection for the people you care about most.

Regular health screenings help catch problems early—often before you notice any symptoms. From heart checks to skin exams, knowing what to look for (and when) can make a huge difference to your long-term health.

If you pass away without a will, your money and belongings may not go to the people you would have chosen. Instead, the law decides who gets what—and the process can be slower, more expensive, and more stressful for your loved ones.

When you take out an insurance policy, it might seem obvious that you own it—but ownership is more than just whose name is on the form. Understanding who owns your policy can affect who gets paid, who can make changes, and how claims are processed.

Insurance policies often come with terms like “exclusions” and “loadings” that can be confusing at first. Understanding what these mean can help you make smarter decisions about your cover and avoid surprises later on.

If someone dies from an accident in New Zealand, ACC offers financial support to help ease the burden on their loved ones. This includes funeral grants, one-off payments, and ongoing income support for dependants.

If you’re injured in an accident, ACC helps cover the cost of treatment, rehabilitation, and time off work—without needing to prove who was at fault. It’s New Zealand’s way of making sure you get support when life takes an unexpected turn.

Mortgage protection and income protection might sound similar, but they serve very different purposes. Knowing the difference helps you choose the right cover to protect your income, your home, or both—depending on your needs.